Introduction

Environmental, Social, and Governance (ESG) and Enterprise Risk Management(ERM) integration is the process of systematically incorporating ESG risks into an organization's ERM framework, ensuring that climate risk, social impact risk, and governance failures are assessed with the same rigor as financial and operational risks.

Environmental, social, and governance risks have moved from the periphery of corporate risk management to its center, driven by a combination of mandatory disclosure requirements, investor scrutiny, and the systemic nature of climate and social risks that do not respect organizational or sector boundaries. The EU's Corporate Sustainability Reporting Directive required the first wave of in-scope companies to apply its reporting rules for FY2024, with disclosures published in 2025, and its phased scope will ultimately reach approximately 50,000 companies globally. ISSB S1 and S2 are now adopted and applying across multiple jurisdictions. The regulatory infrastructure for mandatory ESG disclosure is no longer being built — it is operational.

Yet the gap between disclosure obligation and genuine risk integration remains significant. Many organizations are preparing CSRD-aligned reports without having embedded ESG risks into their enterprise risk management frameworks, creating a disconnect between what is disclosed and what is actually managed. Integrating ESG into ERM closes that gap: it ensures that climate, social, and governance risks are assessed with the same rigor as financial and operational risks, feeding disclosure requirements with real risk data rather than separately assembled sustainability narratives. This article covers why that integration is necessary, what it requires in practice, and how organizations can build an ESG-ERM program that satisfies regulators, informs strategy, and holds up under audit scrutiny.

Questions to consider

• How do you identify, assess, and manage ESG risks of material significance?

• How do you prioritize ESG risks in relation to other enterprise risks?

• Do you assess the impact of ESG risks across your value chain, including your third-party ecosystem?

• Are ESG risks incorporated into financial planning, as well as corporate performance evaluations?

• Is your reporting transparent and clear about the influence of ESG risks on corporate objectives and strategy?

Why Align ESG with ERM?

For years, many Chief Risk Officers (CROs) and Chief Sustainability Officers (CSOs) have operated in silos. But with ESG risks growing more prominent, it’s time to break down these barriers, and operate as one team. The more closely the risk function and the ESG function work together, the better prepared they will be to respond to all kinds of risks.

Here are six reasons to integrate ESG into ERM

ESG is not just a risk, but a BIG one

ESG risks are closely linked to other enterprise risks. For example, the failure to lower carbon emissions could adversely impact a company’s reputation, compliance posture, and financial health. These risk relationships are best understood when ESG risks are mapped to other enterprise risks. The result is a more nuanced risk understanding that can help companies define the scale, scope, and context of their risk management activities. Better risk visibility also allows stakeholders to assess and make more informed decisions about which risks to prioritize and manage.

Use resources more efficiently

When ESG risks are managed as part of a centralized ERM program, companies can enrich risk data while eliminating the duplication of effort, minimizing risk gaps, and optimizing capital allocation.

Strengthen first-line involvement

The people on the front lines are often the best-positioned to spot emerging ESG risks such as a child labor issue in the supply chain. These timely insights can help companies act on ESG risks and opportunities proactively. Therefore, it’s imperative that the first line be involved in ESG risk identification and assessment. Many ERM programs already have clearly defined risk management roles and responsibilities for the first line which ESG teams can easily capitalize on.

Improve risk reporting

ERM taxonomies use a common, consistent language to identify, assess, and report risks. When ESG risks are expressed in these terms, decision-makers can better understand how an ESG issue like unscientific waste management or a lack of employee diversity can impact corporate strategy and objectives. This makes it easier to secure investments for ESG initiatives.

Boost compliance and resilience

Compliance requirements like TCFD recommendations expect companies to incorporate ESG risks into ERM programs. Long-term corporate viability also depends on a company’s ability to predict and respond to all risks and opportunities – including ESG-related ones.

Build trust

Evidence of an integrated risk management program suggests that ESG has been embedded into – and not simply bolted onto – the company’s strategy and operations. Greenwashing concerns are also eliminated when ESG is made part of an established ERM program. It indicates that the company is committed to doing the right thing which, in turn, strengthens credibility with shareholders, investors, and customers.

ESG Regulatory Landscape

| Regulation | Jurisdiction | Current Status | Key Requirements Relevant to ERM |

| CSRD | EU | In force: first wave applied FY2024, reports published 2025; subsequent waves phased through 2029 under revised Omnibus timelines | Double materiality assessment; ESRS-aligned disclosures across environment, social, and governance topics; third-party limited assurance; transition plan for climate |

| ISSB S1 (General Sustainability) | Global (IFRS jurisdictions) | Adopted; applying from 2024 onwards in multiple jurisdictions including UK, Australia, Canada, and Singapore | Disclosure of sustainability-related risks and opportunities using the four-pillar TCFD structure across governance, strategy, risk management, and metrics |

| ISSB S2 (Climate) | Global (IFRS jurisdictions) | Adopted; applying from 2024 onwards; replaces TCFD as the mandatory global climate disclosure standard | TCFD-aligned climate risk disclosure; Scope 1, 2, and 3 GHG emissions; climate scenario analysis under 1.5°C, 2°C, and 4°C pathways |

| SEC Climate Rule | USA | Adopted March 2024; voluntarily stayed by SEC pending legal challenge; defense withdrawn March 2025 under the current administration | Scope 1 and 2 emissions disclosure; material climate risk disclosure in registration statements and annual reports |

| CSDDD | EU | Passed 2024; member state transposition underway through 2025 and 2026 | Human rights and environmental due diligence obligations across value chains; requires active prevention and remediation of negative impacts |

| EU Taxonomy | EU | In force | Classification system for environmentally sustainable economic activities; used in CSRD disclosures to demonstrate alignment of capital with sustainability objectives |

| TCFD | Global | Voluntary framework dissolved in 2023; architectural basis absorbed into ISSB S2, CSRD ESRS E1, and most national climate disclosure requirements | Four-pillar structure: Governance, Strategy, Risk Management, Metrics and Targets; remains the reference framework for most current mandatory climate disclosure regimes |

Get Ahead of ESG Risks by Capitalizing on the Synergies between ESG and ERM

Many companies already have an ERM program to identify, assess, and manage risks. Even in the absence of such a program, companies usually have defined risk management roles, responsibilities, and tasks. These measures provide a starting point for ESG risks to be identified and managed with confidence. Here’s how to capitalize on the synergies between ERM and ESG for better business resilience:

Integrate ESG risks into enterprise risk appetite statements

With environmental and social risks intensifying, it’s important that companies articulate just how much ESG risk they’re willing to tolerate in pursuit of their strategic objectives. For example, eliminating all plastic packaging may be too great a financial risk for an eCommerce company. However, switching to renewable energy may be a more viable option.

These kinds of decisions are easier to make when companies have a good understanding of their ESG risk tolerance levels in the context of their larger enterprise risk appetite. With these insights, stakeholders can then adjust ESG and risk strategies for optimal outcomes. Get Ahead of ESG Risks by Leveraging the Synergies between ESG and ERM

Expand risk registers to include ESG risks

Incorporating ESG risks into existing risk registers does two things. One, it elevates the significance of ESG in senior management discussions. Two, it improves visibility into how ESG risks influence and interact with other enterprise risks.

ESG risks can be identified through a range of methods including risk interviews, online surveys, and risk workshops with investors, customers, and the board.

How well do you know your ESG risks?

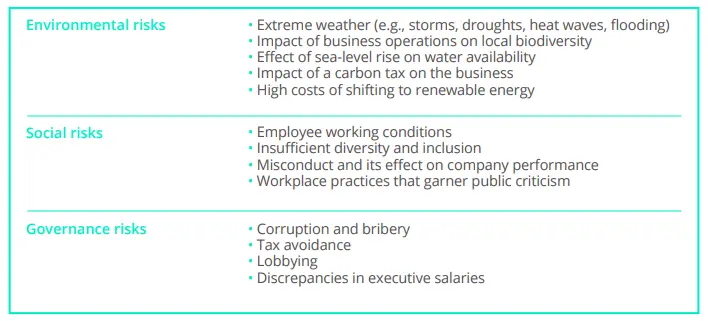

ESG risks range from broad to specific, including:

ESG Risk Categories in ERM Framework

ESG Risk Category ERM Domain Example Risks Assessment Method Relevant Framework Climate Physical Risk Operational and strategic Flooding of facilities, extreme weather disrupting supply chains, water stress affecting manufacturing operations Climate scenario analysis under 1.5°C, 2°C, and 4°C pathways; asset-level physical risk modelling TCFD; ISSB S2; CSRD ESRS E1 Climate Transition Risk Strategic and financial Carbon pricing increasing operating costs, stranded asset exposure, policy changes affecting business model viability Transition scenario modelling; carbon cost sensitivity analysis; portfolio exposure assessment TCFD; ISSB S2; EU Taxonomy Biodiversity and Nature Risk Operational and reputational Deforestation in upstream supply chain, ecosystem dependency for key inputs, land use impacts TNFD framework assessment; supply chain mapping to identify nature-dependent operations CSRD ESRS E4; TNFD Social and Labor Risk Operational and legal Forced or child labor in supply chain, health and safety failures, gender pay gap exposure Human rights due diligence assessments; supplier audits; workforce data analysis CSDDD; CSRD ESRS S1 and S2 Governance Risk Governance and reputational Board composition and independence gaps, executive remuneration misalignment, ethics and anti-corruption failures Board effectiveness assessment; remuneration benchmarking; ethics program review CSRD ESRS G1 AI and Data Privacy Risk Compliance and operational Data breaches affecting personal data of employees or customers, AI model misuse or bias in business decisions Cyber risk assessment integrated with data privacy review; AI governance framework assessment GDPR; EU AI Act Some companies map out their enterprise risks – including ESG risks – at least once a year. This helps them identify which risks need to be addressed on priority.

Many companies also use a single source of risk truth to improve risk visibility. They map ESG risks to other enterprise risks, as well as controls, testing processes, compliance requirements, risk owners, reporting lines and strategic objectives – all in one integrated data model. The result is a holistic risk view that empowers management to make better-informed decisions, and provide better risk oversight.

Improve collaboration between risk management and ESG teams

One of the biggest barriers to ERM-ESG alignment is a lack of communication between risk management and ESG functions. The ESG team doesn’t always speak the same language as the risk team. Equally, risk professionals aren’t often trained to understand, analyze, and respond to ESG risks. This must change if we want to enable a targeted and meaningful approach to ESG risk management.

Many companies have talked about the difficulties of understanding and quantifying ESG risks. These challenges can’t be solved in silos. ESG and ERM teams must work together toward setting risk evaluation standards, best practices, and scoring methodologies that can be equally and consistently applied across all risk types. Since ERM programs already deal with multiple risk types, they must evolve to include ESG risks.

Effective ESG risk management also requires collaboration between ESG teams and other functions, including HR, Legal, and Supply Chain Management. Their collective inputs can help companies build a richer and more nuanced picture of ESG risks in the context of other business risks.

Questions to consider

• Are there opportunities in your company for cross-functional collaboration on ESG risks and issues?

• Is your CSO involved in creating and reviewing the risk register?

• Does the ESG team have a representative on the ERM committee?

• Are ESG terms translated to fit ERM taxonomies?

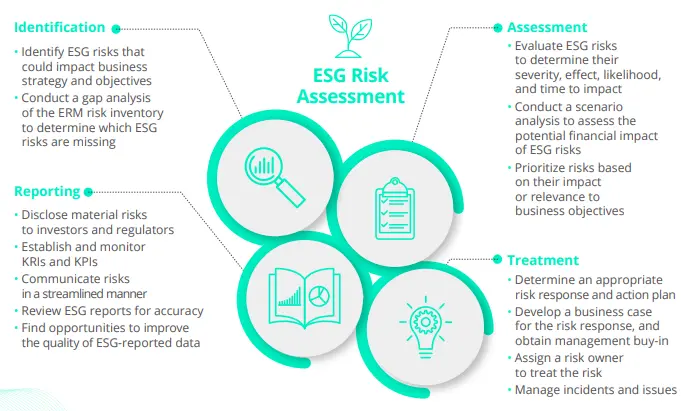

Establish ESG risk management discipline ESG risk management requires a disciplined approach with well-defined roles, responsibilities, and processes. The best way to start is with ERM frameworks like this one issued by COSO and WBCSD. It provides practical guidelines for companies to navigate and manage emerging ESG risks – particularly sustainability risks.ESG risks can be identified and assessed using a range of qualitative and quantitative methods – including a megatrend analysis, SWOT study, ESG materiality assessments, stress testing, and a what-if scenario analysis. These tools, when used as part of an ERM program, help companies understand the severity of ESG risks in relation to other enterprise risks. Management can then prioritize the risks that need the most attention.

CSRD Double Materiality Assessment

Dimension Definition Assessment Process Output Impact Materiality (Inside-Out) Significant actual or potential impacts of the organization's activities on people or the environment, whether positive or negative, intended or unintended Map business activities across the value chain; assess severity, scale, and likelihood of each impact; conduct stakeholder engagement with affected groups and affected communities Ranked list of material impacts with severity and likelihood scores, forming the basis for ESRS disclosure obligations across E, S, and G topics Financial Materiality (Outside-In) ESG topics that generate significant financial risks or opportunities for the organization, affecting cash flows, cost of capital, or access to finance Assess how identified ESG factors could affect the organization's financial position, performance, and cash flows over short, medium, and long-term horizons Ranked list of material ESG risks and opportunities with financial exposure estimates, feeding directly into ERM risk register entries and board risk reporting Double Materiality CSRD requires organizations to assess and disclose on both dimensions; a topic is material under CSRD if it meets either the impact or the financial materiality test Combined analysis integrating both assessments, with cross-referencing to identify topics material on one or both dimensions CSRD-compliant double materiality statement defining the scope of ESRS disclosures required in the sustainability report Risk responses can vary based on a company’s unique risk profile, appetite, and tolerance, as well as the costs and benefits of each response. It helps to have an ESG subject matter expert who can provide insights and guidance on the appropriate risk treatment.

ESG risk management activities must also be reviewed and modified for effectiveness. Well-defined key risk and performance indicators can alert management to any changes in risk identification and response.

Don’t forget third-party ESG risks

Many third-party risk management programs focus on operational disruptions, bribery, corruption, and compliance risks. But ESG risks are equally important, given that an organization’s supply chain can account for more than 90% of its greenhouse gas (GHG) emissions.

Incidents of child labor, worker exploitation, and health and safety issues can also surface across supply chains. Companies have a responsibility to monitor and mitigate these risks through proper third-party screening, periodic risk assessments, and ongoing monitoring and due diligence.

Here's where it helps to integrate ESG with third-party risk management as well as ERM. Having a common platform for all this data can greatly improve risk visibility. It gives management a more nuanced and contextual understanding of ESG risks across their supply chain.

An integrated platform also helps ESG and supply chain governance teams communicate and share data with ease, thus minimizing redundancies and enabling a more holistic approach to third-party ESG risk management.

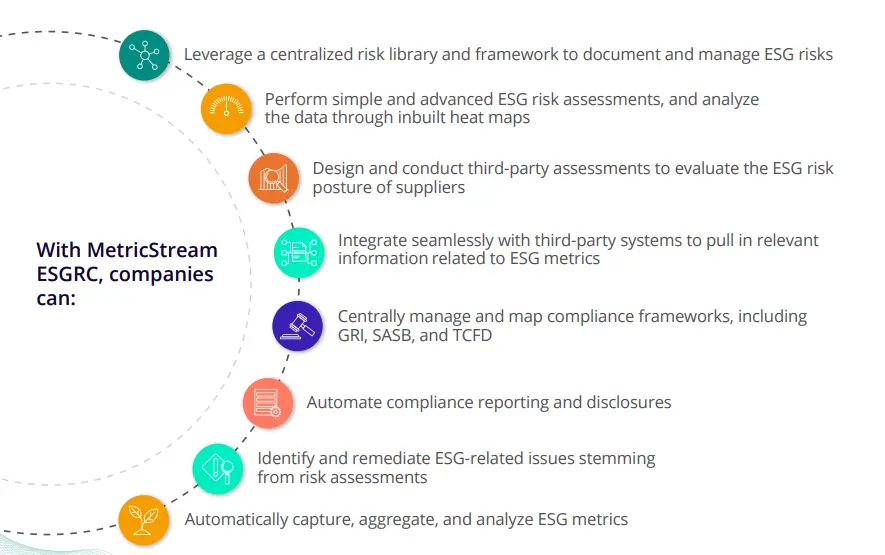

How MetricStream Can Help

At MetricStream, we recognize that ESG isn’t a standalone process. It’s deeply connected to ERM, as well as governance and compliance. When all these elements are managed in an integrated and collaborative manner, companies can reduce risk exposure, drive growth, and strengthen stakeholder confidence.

MetricStream’s AI-native Connected GRC integrates ESG with governance, risk, and compliance (GRC) in one powerful product. It streamlines and automates ESG risk assessment, management, and monitoring across the enterprise and third-party ecosystem, while also simplifying ESG compliance and disclosures.

MetricStream ESGRC is part of our Connected GRC suite of products which enables a holistic approach to ESG, ERM, cyber risk, and multiple other GRC processes.

Discover how MetricStream ESGRC can help you get ahead of ESG risks.

Environmental, Social, and Governance (ESG) and Enterprise Risk Management(ERM) integration is the process of systematically incorporating ESG risks into an organization's ERM framework, ensuring that climate risk, social impact risk, and governance failures are assessed with the same rigor as financial and operational risks.

Environmental, social, and governance risks have moved from the periphery of corporate risk management to its center, driven by a combination of mandatory disclosure requirements, investor scrutiny, and the systemic nature of climate and social risks that do not respect organizational or sector boundaries. The EU's Corporate Sustainability Reporting Directive required the first wave of in-scope companies to apply its reporting rules for FY2024, with disclosures published in 2025, and its phased scope will ultimately reach approximately 50,000 companies globally. ISSB S1 and S2 are now adopted and applying across multiple jurisdictions. The regulatory infrastructure for mandatory ESG disclosure is no longer being built — it is operational.

Yet the gap between disclosure obligation and genuine risk integration remains significant. Many organizations are preparing CSRD-aligned reports without having embedded ESG risks into their enterprise risk management frameworks, creating a disconnect between what is disclosed and what is actually managed. Integrating ESG into ERM closes that gap: it ensures that climate, social, and governance risks are assessed with the same rigor as financial and operational risks, feeding disclosure requirements with real risk data rather than separately assembled sustainability narratives. This article covers why that integration is necessary, what it requires in practice, and how organizations can build an ESG-ERM program that satisfies regulators, informs strategy, and holds up under audit scrutiny.

Questions to consider

• How do you identify, assess, and manage ESG risks of material significance?

• How do you prioritize ESG risks in relation to other enterprise risks?

• Do you assess the impact of ESG risks across your value chain, including your third-party ecosystem?

• Are ESG risks incorporated into financial planning, as well as corporate performance evaluations?

• Is your reporting transparent and clear about the influence of ESG risks on corporate objectives and strategy?

For years, many Chief Risk Officers (CROs) and Chief Sustainability Officers (CSOs) have operated in silos. But with ESG risks growing more prominent, it’s time to break down these barriers, and operate as one team. The more closely the risk function and the ESG function work together, the better prepared they will be to respond to all kinds of risks.

Here are six reasons to integrate ESG into ERM

ESG is not just a risk, but a BIG one

ESG risks are closely linked to other enterprise risks. For example, the failure to lower carbon emissions could adversely impact a company’s reputation, compliance posture, and financial health. These risk relationships are best understood when ESG risks are mapped to other enterprise risks. The result is a more nuanced risk understanding that can help companies define the scale, scope, and context of their risk management activities. Better risk visibility also allows stakeholders to assess and make more informed decisions about which risks to prioritize and manage.

Use resources more efficiently

When ESG risks are managed as part of a centralized ERM program, companies can enrich risk data while eliminating the duplication of effort, minimizing risk gaps, and optimizing capital allocation.

Strengthen first-line involvement

The people on the front lines are often the best-positioned to spot emerging ESG risks such as a child labor issue in the supply chain. These timely insights can help companies act on ESG risks and opportunities proactively. Therefore, it’s imperative that the first line be involved in ESG risk identification and assessment. Many ERM programs already have clearly defined risk management roles and responsibilities for the first line which ESG teams can easily capitalize on.

Improve risk reporting

ERM taxonomies use a common, consistent language to identify, assess, and report risks. When ESG risks are expressed in these terms, decision-makers can better understand how an ESG issue like unscientific waste management or a lack of employee diversity can impact corporate strategy and objectives. This makes it easier to secure investments for ESG initiatives.

Boost compliance and resilience

Compliance requirements like TCFD recommendations expect companies to incorporate ESG risks into ERM programs. Long-term corporate viability also depends on a company’s ability to predict and respond to all risks and opportunities – including ESG-related ones.

Build trust

Evidence of an integrated risk management program suggests that ESG has been embedded into – and not simply bolted onto – the company’s strategy and operations. Greenwashing concerns are also eliminated when ESG is made part of an established ERM program. It indicates that the company is committed to doing the right thing which, in turn, strengthens credibility with shareholders, investors, and customers.

ESG Regulatory Landscape

| Regulation | Jurisdiction | Current Status | Key Requirements Relevant to ERM |

| CSRD | EU | In force: first wave applied FY2024, reports published 2025; subsequent waves phased through 2029 under revised Omnibus timelines | Double materiality assessment; ESRS-aligned disclosures across environment, social, and governance topics; third-party limited assurance; transition plan for climate |

| ISSB S1 (General Sustainability) | Global (IFRS jurisdictions) | Adopted; applying from 2024 onwards in multiple jurisdictions including UK, Australia, Canada, and Singapore | Disclosure of sustainability-related risks and opportunities using the four-pillar TCFD structure across governance, strategy, risk management, and metrics |

| ISSB S2 (Climate) | Global (IFRS jurisdictions) | Adopted; applying from 2024 onwards; replaces TCFD as the mandatory global climate disclosure standard | TCFD-aligned climate risk disclosure; Scope 1, 2, and 3 GHG emissions; climate scenario analysis under 1.5°C, 2°C, and 4°C pathways |

| SEC Climate Rule | USA | Adopted March 2024; voluntarily stayed by SEC pending legal challenge; defense withdrawn March 2025 under the current administration | Scope 1 and 2 emissions disclosure; material climate risk disclosure in registration statements and annual reports |

| CSDDD | EU | Passed 2024; member state transposition underway through 2025 and 2026 | Human rights and environmental due diligence obligations across value chains; requires active prevention and remediation of negative impacts |

| EU Taxonomy | EU | In force | Classification system for environmentally sustainable economic activities; used in CSRD disclosures to demonstrate alignment of capital with sustainability objectives |

| TCFD | Global | Voluntary framework dissolved in 2023; architectural basis absorbed into ISSB S2, CSRD ESRS E1, and most national climate disclosure requirements | Four-pillar structure: Governance, Strategy, Risk Management, Metrics and Targets; remains the reference framework for most current mandatory climate disclosure regimes |

Many companies already have an ERM program to identify, assess, and manage risks. Even in the absence of such a program, companies usually have defined risk management roles, responsibilities, and tasks. These measures provide a starting point for ESG risks to be identified and managed with confidence. Here’s how to capitalize on the synergies between ERM and ESG for better business resilience:

Integrate ESG risks into enterprise risk appetite statements

With environmental and social risks intensifying, it’s important that companies articulate just how much ESG risk they’re willing to tolerate in pursuit of their strategic objectives. For example, eliminating all plastic packaging may be too great a financial risk for an eCommerce company. However, switching to renewable energy may be a more viable option.

These kinds of decisions are easier to make when companies have a good understanding of their ESG risk tolerance levels in the context of their larger enterprise risk appetite. With these insights, stakeholders can then adjust ESG and risk strategies for optimal outcomes. Get Ahead of ESG Risks by Leveraging the Synergies between ESG and ERM

Expand risk registers to include ESG risks

Incorporating ESG risks into existing risk registers does two things. One, it elevates the significance of ESG in senior management discussions. Two, it improves visibility into how ESG risks influence and interact with other enterprise risks.

ESG risks can be identified through a range of methods including risk interviews, online surveys, and risk workshops with investors, customers, and the board.

How well do you know your ESG risks?

ESG risks range from broad to specific, including:

ESG Risk Categories in ERM Framework

ESG Risk Category ERM Domain Example Risks Assessment Method Relevant Framework Climate Physical Risk Operational and strategic Flooding of facilities, extreme weather disrupting supply chains, water stress affecting manufacturing operations Climate scenario analysis under 1.5°C, 2°C, and 4°C pathways; asset-level physical risk modelling TCFD; ISSB S2; CSRD ESRS E1 Climate Transition Risk Strategic and financial Carbon pricing increasing operating costs, stranded asset exposure, policy changes affecting business model viability Transition scenario modelling; carbon cost sensitivity analysis; portfolio exposure assessment TCFD; ISSB S2; EU Taxonomy Biodiversity and Nature Risk Operational and reputational Deforestation in upstream supply chain, ecosystem dependency for key inputs, land use impacts TNFD framework assessment; supply chain mapping to identify nature-dependent operations CSRD ESRS E4; TNFD Social and Labor Risk Operational and legal Forced or child labor in supply chain, health and safety failures, gender pay gap exposure Human rights due diligence assessments; supplier audits; workforce data analysis CSDDD; CSRD ESRS S1 and S2 Governance Risk Governance and reputational Board composition and independence gaps, executive remuneration misalignment, ethics and anti-corruption failures Board effectiveness assessment; remuneration benchmarking; ethics program review CSRD ESRS G1 AI and Data Privacy Risk Compliance and operational Data breaches affecting personal data of employees or customers, AI model misuse or bias in business decisions Cyber risk assessment integrated with data privacy review; AI governance framework assessment GDPR; EU AI Act Some companies map out their enterprise risks – including ESG risks – at least once a year. This helps them identify which risks need to be addressed on priority.

Many companies also use a single source of risk truth to improve risk visibility. They map ESG risks to other enterprise risks, as well as controls, testing processes, compliance requirements, risk owners, reporting lines and strategic objectives – all in one integrated data model. The result is a holistic risk view that empowers management to make better-informed decisions, and provide better risk oversight.

Improve collaboration between risk management and ESG teams

One of the biggest barriers to ERM-ESG alignment is a lack of communication between risk management and ESG functions. The ESG team doesn’t always speak the same language as the risk team. Equally, risk professionals aren’t often trained to understand, analyze, and respond to ESG risks. This must change if we want to enable a targeted and meaningful approach to ESG risk management.

Many companies have talked about the difficulties of understanding and quantifying ESG risks. These challenges can’t be solved in silos. ESG and ERM teams must work together toward setting risk evaluation standards, best practices, and scoring methodologies that can be equally and consistently applied across all risk types. Since ERM programs already deal with multiple risk types, they must evolve to include ESG risks.

Effective ESG risk management also requires collaboration between ESG teams and other functions, including HR, Legal, and Supply Chain Management. Their collective inputs can help companies build a richer and more nuanced picture of ESG risks in the context of other business risks.

Questions to consider

• Are there opportunities in your company for cross-functional collaboration on ESG risks and issues?

• Is your CSO involved in creating and reviewing the risk register?

• Does the ESG team have a representative on the ERM committee?

• Are ESG terms translated to fit ERM taxonomies?

Establish ESG risk management discipline ESG risk management requires a disciplined approach with well-defined roles, responsibilities, and processes. The best way to start is with ERM frameworks like this one issued by COSO and WBCSD. It provides practical guidelines for companies to navigate and manage emerging ESG risks – particularly sustainability risks.ESG risks can be identified and assessed using a range of qualitative and quantitative methods – including a megatrend analysis, SWOT study, ESG materiality assessments, stress testing, and a what-if scenario analysis. These tools, when used as part of an ERM program, help companies understand the severity of ESG risks in relation to other enterprise risks. Management can then prioritize the risks that need the most attention.

CSRD Double Materiality Assessment

Dimension Definition Assessment Process Output Impact Materiality (Inside-Out) Significant actual or potential impacts of the organization's activities on people or the environment, whether positive or negative, intended or unintended Map business activities across the value chain; assess severity, scale, and likelihood of each impact; conduct stakeholder engagement with affected groups and affected communities Ranked list of material impacts with severity and likelihood scores, forming the basis for ESRS disclosure obligations across E, S, and G topics Financial Materiality (Outside-In) ESG topics that generate significant financial risks or opportunities for the organization, affecting cash flows, cost of capital, or access to finance Assess how identified ESG factors could affect the organization's financial position, performance, and cash flows over short, medium, and long-term horizons Ranked list of material ESG risks and opportunities with financial exposure estimates, feeding directly into ERM risk register entries and board risk reporting Double Materiality CSRD requires organizations to assess and disclose on both dimensions; a topic is material under CSRD if it meets either the impact or the financial materiality test Combined analysis integrating both assessments, with cross-referencing to identify topics material on one or both dimensions CSRD-compliant double materiality statement defining the scope of ESRS disclosures required in the sustainability report Risk responses can vary based on a company’s unique risk profile, appetite, and tolerance, as well as the costs and benefits of each response. It helps to have an ESG subject matter expert who can provide insights and guidance on the appropriate risk treatment.

ESG risk management activities must also be reviewed and modified for effectiveness. Well-defined key risk and performance indicators can alert management to any changes in risk identification and response.

Don’t forget third-party ESG risks

Many third-party risk management programs focus on operational disruptions, bribery, corruption, and compliance risks. But ESG risks are equally important, given that an organization’s supply chain can account for more than 90% of its greenhouse gas (GHG) emissions.

Incidents of child labor, worker exploitation, and health and safety issues can also surface across supply chains. Companies have a responsibility to monitor and mitigate these risks through proper third-party screening, periodic risk assessments, and ongoing monitoring and due diligence.

Here's where it helps to integrate ESG with third-party risk management as well as ERM. Having a common platform for all this data can greatly improve risk visibility. It gives management a more nuanced and contextual understanding of ESG risks across their supply chain.

An integrated platform also helps ESG and supply chain governance teams communicate and share data with ease, thus minimizing redundancies and enabling a more holistic approach to third-party ESG risk management.

At MetricStream, we recognize that ESG isn’t a standalone process. It’s deeply connected to ERM, as well as governance and compliance. When all these elements are managed in an integrated and collaborative manner, companies can reduce risk exposure, drive growth, and strengthen stakeholder confidence.

MetricStream’s AI-native Connected GRC integrates ESG with governance, risk, and compliance (GRC) in one powerful product. It streamlines and automates ESG risk assessment, management, and monitoring across the enterprise and third-party ecosystem, while also simplifying ESG compliance and disclosures.

MetricStream ESGRC is part of our Connected GRC suite of products which enables a holistic approach to ESG, ERM, cyber risk, and multiple other GRC processes.

Discover how MetricStream ESGRC can help you get ahead of ESG risks.

Frequently Asked Questions

ESG and ERM integration means incorporating climate, social, and governance risks into the enterprise risk management framework so they are assessed with the same rigor as financial and operational risks and connected directly to mandatory sustainability disclosures.

CSRD requires assessing both impact materiality, whether the organization's activities harm people or the environment, and financial materiality, whether ESG factors create financial risk or opportunity, with a topic being material under CSRD if either test is met.

As of June 2026, CSRD applies to the first wave of EU companies from FY2024, ISSB S1 and S2 are adopted across multiple jurisdictions, CSDDD passed in 2024, and the SEC Climate Rule remains stayed pending legal challenge.

Climate risk should be integrated using TCFD's four pillars as the structural framework, with physical and transition risks identified under defined climate scenarios, mapped to the enterprise risk register, and disclosed per ISSB S2 and CSRD ESRS E1.

Scope 1 covers direct emissions from owned sources, Scope 2 covers indirect emissions from purchased energy, and Scope 3 covers all value chain emissions, which typically represent 70 to 90% of total footprint and are required under CSRD and ISSB S2.

CSRD is the EU's mandatory sustainability reporting framework, in force from FY2024 for the first wave of companies, requiring double materiality assessment, ESRS-aligned disclosures across environment, social, and governance topics, a climate transition plan, and limited third-party assurance.

ESG factors are now embedded in Moody's, S&P, and Fitch rating methodologies, meaning weak ESG risk management profiles translate directly into higher borrowing costs, exclusion from ESG-screened investment portfolios, and reduced valuations for affected organizations.

TCFD established the four-pillar climate disclosure framework in 2017 and dissolved in 2023, but remains directly relevant as the architectural basis for ISSB S2, CSRD ESRS E1, and most national mandatory climate disclosure frameworks currently in force.

Integrating ESG into a risk register follows four steps: identify material ESG risks through a double materiality assessment, score them using the existing risk methodology calibrated for ESG dimensions, assign owners and controls, and map entries to CSRD and ISSB disclosure requirements.

ESG integration into a risk register requires identifying material risks through a double materiality assessment, scoring them using the existing methodology, assigning owners and controls, and mapping each entry to the applicable CSRD and ISSB disclosure requirements.

MetricStream provides ESG risk management within the broader ERM framework, double materiality assessment workflows, CSRD-aligned disclosure processes, climate scenario analysis for ISSB S2, and simultaneous mapping to ESRS, TCFD, ISSB S1 and S2, and GRI.