Banking and financial services (BFS) risk leaders are navigating one of the most demanding environments in recent memory. Regulatory scrutiny is intensifying across every jurisdiction. AI adoption is accelerating inside institutions at a pace that governance frameworks were never designed to match. Fraud is no longer just a human problem – AI-powered scams, deepfakes, and synthetic identity attacks are now mainstream threats. And the financial consequences of getting it wrong? Steep. In 2025, financial services faced an average data breach cost of $5.56 million, the second highest after healthcare ($7.42M), per IBM's Cost of a Data Breach Report 2025.

Against this backdrop, the question for risk and compliance leaders is no longer whether to modernize their GRC approach; it is how fast they can make the shift, and whether their organizations are building the right foundations to make it stick.

Legacy GRC frameworks were built for a different era. They assumed risks could be managed in silos, that periodic assessments would surface emerging threats in time, and that static controls could hold against a relatively stable regulatory landscape. None of those assumptions hold good today.

Modern risk events do not respect organizational boundaries. A third-party outage can trigger a cyber incident, which triggers a regulatory notification requirement, which surfaces a data quality gap that was already undermining your AI model outputs. These cascading and cross-domain failures are increasingly the norm, and they expose a fundamental flaw in siloed, manual, retrospective GRC operations.

Regulators have taken notice of this - across the U.S., UK, and EU, supervisory bodies are moving away from accepting policy documentation as evidence of compliance. They now expect institutions to demonstrate integrated governance, real-time awareness of risk posture, and board-level accountability for outcomes. Frameworks like the EU AI Act, DORA, and evolving guidance from the FCA and Fed are converging around a single expectation: your governance must be as dynamic as your risk environment.

AI is not a future consideration for GRC. It is already reshaping how leading institutions identify risk, manage compliance obligations, and run governance workflows. The transformation is playing out across three interconnected dimensions.

A. AI for Actionable Risk Insights

The most immediate impact of AI in GRC is the shift from backward-looking reporting to forward-looking risk intelligence. AI-enabled platforms can simultaneously ingest structured and unstructured data across risk domains — market signals, control test results, third-party performance data, cyber threat feeds, and continuously analyze that information for patterns and anomalies that would be impossible for human analysts to surface in time.

Risk management stops being a function that reports what happened and becomes one that anticipates what is about to happen.

B. AI for Continuous Compliance

The compliance burden in banking has grown faster than compliance teams could keep headcounts for years. AI addresses this gap directly. Regulatory change management, historically a labor-intensive process of tracking updates across dozens of jurisdictions and mapping them to internal policies and controls, can now be substantially automated. AI tools can monitor regulatory publications in real time, flag relevant changes, and propose policy-to- control alignment updates for human review and approval. Equally transformative is the elimination of evidence-chasing. A significant portion of compliance teams’ time in traditional GRC environments is spent manually collecting documentation to satisfy audit and regulatory requests.

The final result is a compliance function that is genuinely continuous rather than episodic — one that maintains readiness every day, not just in the weeks before an assessment.

C. AI Agents in Connected, Continuous, and Cognitive GRC

With the emergence of agentic AI, GRC systems can execute multi-step tasks autonomously within defined boundaries. They are beginning to reshape GRC workflows at their most granular level. Agents can handle workflow routing, ensuring that risk findings reach the right owners without manual intervention. They can pre-populate risk and control assessments based on historical data and contextual signals. Across approval chains, they reduce manual clicks and accelerate remediation cycles by surfacing relevant guidance and suggested next actions at exactly the right moment.

The result is a GRC environment that is not just connected and continuous, but genuinely cognitive. One where the platform actively participates in risk management. That said, the human-in-the-loop is not optional. It is a regulatory expectation and operational necessity.

There is an important paradox at the center of AI adoption in banking: the technology being deployed to strengthen risk management is itself a significant and growing source of risk. AI systems can hallucinate, encode bias, produce opaque outputs, and be exploited by adversaries who understand their failure modes better than their operators do. According to Deloitte, losses from AI-powered fraud alone could reach $40 billion in the US by 2027.

Responsible AI in financial services is not just a compliance and ethics conversation. Institutions must maintain a comprehensive inventory of AI use cases across the organization, establish model validation and ongoing monitoring requirements, and embed human oversight into any AI-assisted decision that touches regulated outcomes such as credit assessment, fraud detection, or capital allocation.

Underlying all of this is data quality. AI governance cannot be separated from data governance. Organizations with fragmented data architectures will find their AI investments constrained by unreliable outputs and their regulatory relationships strained by an inability to explain where their numbers come from. Clean, well-governed data is not a prerequisite to start the AI journey, but a prerequisite to scaling it with confidence.

The contrast between traditional and AI-first approaches to GRC is significant across every operational dimension:

| Dimension | Traditional GRC | AI-First Connected GRC |

| Architecture | Manual, siloed | Unified, data-driven |

| Posture | Reactive | Predictive |

| Monitoring | Periodic (point-in-time) | Continuous (real-time) |

| Workflow | Evidence chasing | Insight generation |

| Risk Visibility | Fragmented, static | Holistic, dynamic |

| Reporting | Backward-looking | Forward-looking |

| Resource Burden | High (manual effort) | Reduced (automated workflows) |

| Decision-Making | Intuition-driven | Insight-driven |

For BFS leaders, 2026 demands a clear-eyed assessment of where GRC capabilities stand and a concrete roadmap for closing the gap. Building enterprise resilience against interconnected risk scenarios, embedding AI into risk intelligence and compliance workflows in a governed and phased way, strengthening third-party oversight across increasingly AI-dependent vendor ecosystems, and unifying compliance management across jurisdictions, these are the priorities that will separate leading institutions from lagging ones over the next 12 to 18 months. Below is a quick snap of priorities for the banking and financial sector:

In our latest eBook, 7 Strategic Priorities for Banking and Financial Services in 2026, we outline how leading institutions are embedding AI within Connected GRC frameworks to strengthen governance, resilience, and regulatory readiness, and what BFS leaders need to do right now to stay ahead.

Gaurav Kapoor, Vice Chairman and Co-Founder of MetricStream, recently sat down with Debbie Forster, MBE on the XTech Podcast, to talk all things GRC and AI. Drawing on decades of experience — from launching one of India's first internet-based consumer remittance products in the mid-90s to leading an AI-first transformation at MetricStream today — Gaurav shares candid insights on the evolving GRC landscape, AI's role in risk management, cybersecurity threats, and what it really means to govern AI itself.

The XTech Podcast brings together leading voices from across the global tech community to cut through the complexity of today's most pressing innovations.

Gaurav's career is a masterclass in turning disruption into opportunity. From 9/11 and the Enron scandal to the 2008 financial crisis and COVID-19, each major crisis exposed the same fundamental problem: siloed organisations where critical risk data wasn't being shared across functions.

"One part of the organisation wasn't talking to the other part. If you can bring all this together, the opportunity for the organisation to see risk holistically changes the paradigm."

The lesson? The organisations that thrive are the ones that treat crisis not as an anomaly, but as a signal to act on what they already knew needed fixing.

For years, GRC lagged behind other functions like sales and finance in adopting AI and for understandable reasons. As Gaurav explains, a 90% accuracy rate is fine in marketing; it's not acceptable in risk management, where a missed signal can mean a billion-dollar regulatory fine.

But the landscape has shifted. The canvas of risk has expanded dramatically. It now spans cyber threats, geopolitical shifts, supply chain vulnerabilities, and the risks introduced by AI itself. The volume and complexity of risk information have simply become too great to manage manually. AI is no longer optional; it's essential.

Gaurav explains how MetricStream's AI-first strategy wasn't driven by technology for technology's sake. It was grounded in a clear-eyed diagnosis of what GRC professionals actually struggle with every day:

MetricStream's response was to use AI to automate the rote work, freeing practitioners to focus on higher-value, domain-specific thinking. The new company tagline says it plainly: "GRC Simplified. Outcomes Amplified."

Will AI replace GRC professionals? Gaurav's answer is nuanced. He shared the perspective of a Chief Auditor at one of the world's largest oil and gas companies, who said he would actually need more auditors in an AI-enabled world.

Why? Because, according to him, his auditors are the brain trust of the organisation. With AI handling sample testing and routine execution, they could move to 100% population testing and explore risks that were previously invisible.

Gaurav's framework: Assist Augment Delegate. GRC AI is moving through these phases progressively, with full delegation still some way off as models become more reliable. The professionals who will thrive are those who deepen their domain expertise and embrace AI as a force multiplier.

As AI takes on more of the work of governance, who governs the AI? Gaurav highlights three critical dimensions:

On cybersecurity, Gaurav made a striking observation: the fortresses have strengthened, but the ecosystems have weakened. Attackers have adapted, shifting from targeting organisations directly to infiltrating their extended partner and supply chain networks.

His example was pointed: one of the world's largest payment networks — with world-class cybersecurity — was breached via a compromised small retailer in Indonesia, a breach that could have threatened the stability of the entire financial system.

"It could come from anywhere."

Third-party and supply chain risk management is no longer a secondary concern. It sits at the heart of enterprise resilience.

When asked what he's reading, Gaurav pointed to Nassim Nicholas Taleb's The Black Swan and Antifragile — books he has returned to with renewed appreciation. The core idea: build systems that don't just survive shocks, but get stronger from them, by deliberately simulating disruptions before they happen.

In a world where the next crisis could arrive on a Tuesday rather than a distant horizon, building anti-fragile organisations is a strategic imperative.

GRC is undergoing a fundamental transformation. The combination of expanding risk complexity, accelerating regulatory pressure, and maturing AI capabilities means that the old model of manual, reactive, and siloed risk management is no longer fit for purpose. The organisations that will lead are those that embed AI into Connected GRC frameworks — not just for efficiency, but for the foresight and strategic risk intelligence that drives growth.

Discover how MetricStream is helping organisations simplify governance, strengthen resilience, and amplify outcomes with Connected GRC.

Explore MetricStream’s AI-first Connected GRC. Request a demo.

The start of a new year creates a natural pause. Personally, for me, the New Year is a moment to step back, take stock, and recalibrate priorities.

This holds true for organizations across sectors running governance, risk, and compliance (GRC) programs as well; it’s an opportunity to reassess their resilience strategies in the face of an increasingly complex world.

As organizations prepare to strengthen their capabilities and harness the transformative potential of cutting-edge technologies, they will need to continue to brace for the unknown unknowns driven by a host of factors, including geopolitical conflicts, economic uncertainty, intensifying cyber threats, supply-chain disruptions, and evolving regulatory demands. According to several recent global risk assessments, including the IIA’s Risk in Focus report and the Allianz Risk Barometer, geopolitical uncertainty and digital disruption, along with cyber risk, are the top concerns among practitioners and leaders worldwide. So, while leadership and top management review the past year and chalk out business goals and strategies for the year ahead, GRC leaders should take this opportunity to rethink their approach and implement changes in processes, tools, and technologies that will boost their organization’s resilience.

Against this backdrop, here are 10 key risk and compliance resolutions for GRC leaders to help successfully navigate 2026.

AI governance can no longer stop at principles and policies. In 2026, risk and compliance leaders should focus on operationalizing AI governance end-to-end by maintaining an enterprise inventory of AI use cases, embedding risk and compliance checks into model and product lifecycles, and implementing ongoing monitoring and observability. The goal is to ensure AI risks are actively managed in production and governance outcomes are clearly tied to business performance, trust, and resilience.

Cyber risk needs to be framed in terms that boards and executives can act on. This means translating technical vulnerabilities into business impact, such as financial loss, operational disruption, customer harm, and regulatory exposure. By quantifying cyber risk and aligning it with the enterprise risk appetite, GRC leaders can enable more informed decision-making and better prioritize security investments.

Agentic and autonomous AI systems are rapidly being used in the real world. Risk, compliance, audit and cyber risk agents are capable of autonomously monitoring risks, orchestrating controls, initiating remediation, and escalating issues. To realize this value responsibly, GRC leaders must define clear mandates for what agents can and cannot do, embedding human-in-the-loop oversight for critical judgments, and establishing governance guardrails around access, testing, and escalation.

Point-in-time assessments and annual reviews are no longer sufficient in a fast-moving risk environment. Organizations should move toward continuous risk and compliance assessments leveraging real-time data feeds, automated control testing, and dynamic risk indicators. This shift enables earlier detection of issues, faster remediation, and greater confidence in the organization’s risk posture between audits.

Regulations such as DORA and NIS2 signal a clear shift from compliance checklists to demonstrated operational resilience. Risk and compliance programs should integrate scenario testing, recovery objectives, and third-party resilience directly into their workflows. By aligning compliance efforts with measurable resilience outcomes, organizations can meet regulatory expectations while strengthening their ability to withstand disruption.

Manual, spreadsheet-driven compliance processes create inefficiency, increase error, and limit scalability. In 2026, organizations should prioritize integrated and automated GRC platforms that connect risk, compliance, IT, security, and third-party systems. Automation not only accelerates evidence collection and reporting but also frees teams to focus on higher-value risk analysis and decision support.

Third-party and supply-chain risks remain a top concern, particularly for critical and technology-dependent services. Leading organizations are moving beyond periodic assessments to continuous monitoring, concentration risk analysis, and stronger contractual requirements for resilience and transparency. Where risk is elevated, oversight must extend beyond direct vendors to key sub-service providers.

Traditional GRC metrics often focus on activity volume, including the number of controls tested, issues logged, or assessments completed. In 2026, leaders should emphasize outcome-based KPIs that demonstrate real impact, such as reductions in unmitigated risk, faster containment of control failures, and increased automation of critical controls. These metrics help clearly articulate the value of GRC to executive stakeholders.

As AI becomes embedded in risk, compliance, and business decision-making, explainability and auditability are no longer optional. Organizations should institutionalize documentation, model lineage, decision logs, and testing artifacts across the AI lifecycle. This ensures AI-driven outcomes can be explained to regulators, auditors, customers, and internal stakeholders with confidence.

Fragmented ownership and duplicative compliance efforts continue to slow organizations down. GRC leaders should work toward unified risk taxonomies, shared control libraries, and a single source of truth across functions. At the same time, controls and evidence should be designed once and reused across overlapping regulations, such as DORA, NIS2, SEC cyber rules, and local mandates, leading to reduced complexity and improved efficiency.

2026 will test how effectively risk and compliance programs move from oversight to enablement, supporting innovation while protecting the organization from emerging risks. For GRC leaders, this moment calls for strong resolutions.

All the best with your 2026 risk and compliance resolutions! And here’s to a year of building stronger, more resilient organizations.

Need help on your GRC Journey? Request a personalized demo today.

In an era of constant disruption, organizations must evolve their risk management strategies to stay resilient and responsive. MetricStream, in collaboration with RSM, recently hosted a webinar to discuss how Enterprise Risk Management (ERM) is transforming—and what the future demands of it. From dynamic risk assessments to the intelligent use of technology, here are the core insights that we covered.

Watch the webinar recording: Rethinking ERM: A Strategic Imperative for the Future

One of the central themes we discussed was the importance of making risk appetite statements more dynamic and aligned with actual business operations and strategic business objectives. Traditionally, these statements were generic, high-level, and rarely reflected the nuances at the business unit or process level.

There is immense value in weighted risk aggregation, where organizations assign importance to different dimensions—such as business units, geography, and product lines. This approach offers a more accurate picture of risk exposure and ensures risk appetite is tailored, not templated. It also helps eliminate the guesswork by incorporating data-driven insights into how much risk a specific business area can or should tolerate. Moreover, collaboration across risk owners in both the first and second lines of defense is critical to ensure that risk appetite statements remain practical and fully aligned with business objectives and strategy.

Static, periodic risk assessments no longer will suffice in today’s volatile environment. Risks emerge and evolve too quickly for annual or quarterly reviews to be effective. There is an urgent need to move toward continuous and real-time assessments.

Traditional assessments often operate in silos, rely heavily on lagging indicators, and assume too much confidence in manual controls. In contrast, dynamic risk assessments enable faster detection of emerging threats, more responsive decision-making, and integrated oversight across business lines. This shift ensures risk management becomes a living, breathing process that evolves in conjunction with the business. Breaking down silos is essential; a unified risk inventory and taxonomy enables organizations to consolidate risk assessments across business units and facilitates real-time visibility. Furthermore, establishing feedback loops following risk events ensures that the risk assessment process is continually refined and remains responsive to change.

A recurring point we touched upon was the growing importance of risk quantification—particularly when it comes to non-financial risks. Quantifying risk exposure in monetary terms helps bridge the gap between risk management and strategic planning, two crucial concepts.

Organizations, especially in regulated sectors like financial services, are increasingly expressing risks as potential loss ranges (e.g., minimum, maximum, and average exposures). This allows decision-makers to better understand the impact, prioritize mitigation efforts, and ensure capital adequacy. It also supports more rigorous scenario planning and better alignment with board-level discussions. In addition to quantifying risks, integrating robust scenario analysis—including stress testing for emerging risks—provides deeper insights into potential risk exposures and supports more comprehensive risk-informed decision-making.

No modern ERM strategy is complete without a strong technology foundation. Today’s risk environments demand systems that are agile, intelligent, and user driven. Tools like MetricStream empower risk teams to automate workflows, send real-time surveys and assessments, and analyze incoming risk data without relying heavily on outdated IT systems or processes, which is an added bonus around data integrity.

Features like AI-powered chatbots or risk reporting assistants allow frontline employees to flag concerns instantly—even anonymously if needed. This democratization of risk intelligence ensures that signals from the ground level are captured early and acted upon quickly. Modern ERM platforms further empower business users through low-code/no-code solutions that allow frontline risk owners to create, adjust, and deploy risk surveys and dashboards without any additional IT dependency. Technology also supports better collaboration between the first and second lines, providing real-time visibility into the risk landscape across the enterprise.

Governance was another area we focused on, particularly the need to move away from a “check-the-box” mentality. Effective governance is not about adding oversight committees or rigid frameworks—it’s about fostering partnership across the three lines of defense.

A successful ERM program encourages leadership to engage directly with business units, making risk discussions part of operational decision-making. Transforming governance into a collaborative partnership among all levels of management reinforces a proactive risk culture and ensures that risk ownership is a shared responsibility.

When senior management supports this integration, it becomes easier to cultivate a risk-aware culture where everyone—from executives to frontline staff—feels accountable for identifying and managing risk and it is no longer the sole responsibility of a group of individuals.

We emphasized that ERM should no longer be viewed solely as a compliance function. When implemented dynamically and supported by technology, it becomes a strategic enabler—one that enhances agility, informs decision-making, and provides a competitive edge.

As the webinar poll results revealed, the journey from “somewhat” to “very” confident in the ERM maturity journey is about incremental progress. It involves embedding risk into the business's rhythm, leveraging real-time data, and empowering teams with the right tools and governance structures.

The future of ERM lies in integration, intelligence, and innovation. By aligning risk appetite with business objectives and strategy, adopting continuous risk and control assessments, quantifying exposures, and leveraging smart technologies, organizations can transform risk management from a siloed process into a core strategic function. ERM done right isn’t just about avoiding risk but about thriving through it.

Watch the webinar recording for more insights:

In today’s rapidly evolving world, the risk landscape is changing faster than ever. We’ve witnessed firsthand the mounting challenges organizations face with an increasingly complex web of regulatory requirements, cyber threats, and operational resilience. The issues organizations face today are more interconnected, urgent, and nuanced than ever before.

As we reflect on the insights from a recent survey conducted by MetricStream and the GRC Report, which polled over 100 global GRC professionals, five critical areas stand out as key learnings for organizations in 2025. These insights offer not only a roadmap for navigating the complexities ahead but also a chance to transform challenges into opportunities for growth and competitive advantage.

Regulatory complexity, especially the speed of regulatory changes, remains a top concern, with 51% of professionals citing it as a pressing challenge. The pace of these changes is accelerating, and many organizations struggle with resource constraints—both in terms of personnel and expertise—just to keep up. The solution? Strengthening compliance management frameworks, leveraging technology to streamline processes, and integrating regulatory intelligence into decision-making. The goal should be to view compliance not as a checkbox exercise but as a catalyst for competitive advantage and operational excellence.

Cyber risk remains a moving target, with nearly 48% of GRC professionals identifying it as a critical priority. Interestingly, only 8% of survey respondents were cybersecurity professionals, while the majority came from compliance, audit, integrated risk, and risk management roles. This underscores the urgent need for a broader, organization-wide focus on managing cyber risk. While companies are doubling down on real-time threat intelligence, continuous control monitoring, and advanced AI-driven threat detection, organizations must embed cyber risk into their broader risk management strategy, ensuring that resilience is built into every level of operations.

Artificial Intelligence is front and center in GRC conversations, with 47% of respondents viewing it as both an opportunity and a challenge. Organizations are realizing the potential of AI to revolutionize risk management—automating processes, detecting anomalies, and predicting emerging threats. However, the risks associated with unchecked AI adoption—including ethical concerns, bias in decision-making, and integration complexities—must be carefully addressed. To harness AI effectively, organizations need to establish governance frameworks that ensure transparency, accountability, and data integrity. The key is responsible AI adoption—leveraging its strengths while mitigating its risks.

Nearly 46% of GRC professionals are prioritizing resilience as a core business strategy, largely driven by the stronger regulatory push to build operational resilience. In my experience, organizations that treat resilience as a forward-looking capability that integrates seamlessly with operational risk management—rather than just a compliance requirement—are the ones that emerge stronger in the face of crises. As we’ve mentioned earlier, resilience must become part of an organization’s DNA. This means embedding resilience into daily operations, stress-testing response plans, and ensuring that every employee understands their role in mitigating risk.

A fragmented approach to risk management is one of the biggest barriers to effective GRC. Over 42% of professionals in the survey emphasized the need for an integrated risk framework. When asked what their biggest concerns for GRC and risk were as they plan for 2025, one respondent said, “Breaking down silos between risk, compliance, and operations teams to improve collaboration,” while another noted, “A lack of collaboration among GRC professionals.” We’ve long advocated for breaking down silos between risk, compliance, audit, and cybersecurity teams to create a unified view of risk. Organizations need to build a risk culture where collaboration is the norm, data flows seamlessly across functions, and risk intelligence informs strategy at every level.

As we look to 2025, the role of GRC professionals will be more critical than ever. In a world that is increasingly complex, interconnected, and constantly evolving, the future of GRC lies not just in managing risk, but in strategically positioning organizations to thrive amid uncertainty.

By tackling these challenges head-on, GRC leaders will shape organizations that are not only resilient but innovative, prepared to lead in an era of constant change. These insights aren’t just about surviving, they are about setting a course for success in 2025 and beyond.

Watch the webinar recording for a deep-dive discussion of the survey results:

Do you believe in New Year’s resolutions?

In my personal life, I usually make one or two big changes every January—and they’ve mostly (!) held. A new year is a great time for fresh starts, bold aspirations, and a renewed focus on change, growth, and innovation.

That holds true for companies and industries – especially in governance, risk, and compliance (GRC). Across industries, organizations are gearing up to tackle challenges head-on, enhance their capabilities, and embrace the transformative potential of cutting-edge technologies. Organizations are bracing themselves for the unknown unknowns stemming from escalating geo-political conflicts in various parts of the world, a volatile economic outlook, intensifying cyber risks, severe supply chain disruptions, an array of new regulations, and more

According to the World Economic Forum’s 2025 Global Risks Report, “the overall view of global risks is much the same as last year if more negatively weighted.” Along with spotlighting extreme weather events, increasing misinformation, and cyber attacks, the report also highlighted ‘the adverse outcomes of AI technologies’ as a risk to be expected in the long term.

So, while leadership and top management review the past year and chalk out business goals and strategies for the year ahead, GRC leaders should take this opportunity to rethink their approach and implement changes in processes, tools, and technologies that will boost their organization’s resilience.

Against this backdrop, here are 5 key risk and compliance resolutions for organizations to help successfully navigate 2025. What are yours? Let us know in the comments!

Risk is an inherent part of business. Instead of viewing risk as detrimental to the organization’s growth and financial posture, GRC leaders should look to turn risks into opportunities. The willingness to take risks can help organizations gain a competitive edge and drive greater profitability and business value. However, there’s a catch—not all risks translate into strategic advantage. So, how can organizations decide whether to accept, reject, avoid, or mitigate a risk?

This is where the risk management program comes into play. An effective risk management program can enable decision-makers to make well-informed business decisions by providing a streamlined process for evaluating opportunities. It equips the top management and leadership with actionable insights, improved risk visibility and foresight, and greater transparency that helps them better manage projects based on risk impact and probability in relation to potential return.

Explore the top risk and compliance trends for 2025: GRC Forecast for 2025: 7 Must-Know Trends

In just the second quarter of 2024, cyberattacks worldwide shot up by 30%, reaching 1,636 attacks per organization per week, according to Check Point Research.

To protect their IT and cyber infrastructure from frequent and increasingly sophisticated cyber attacks, organizations need to level up their cyber risk management approach. Relying on periodic reviews and assessments of cyber risks and controls is no longer enough. Organizations need an automated, autonomous, and continuous approach that enables them to proactively identify and address any risks, threats, vulnerabilities, control weaknesses/gaps, and issues before they snowball into something significant.

Organizations today can also harness the power of artificial intelligence (AI) and other advanced technologies to improve risk management processes and enhance efficiency. AI can significantly accelerate the decision-making process by quickly providing insights into risk trends and patterns as well as identifying areas of improvement – such as the number of duplicate or redundant controls, patterns of over and under-testing of controls, optimum control testing frequency, similar issues, and more.

Discover the upcoming cyber shifts in 2025: 10 Cyber GRC Trends to Watch in 2025

Regulatory compliance is becoming an increasingly challenging and demanding business function for organizations worldwide.

The year 2024 witnessed significant regulatory advancements, with a strong emphasis on resilience, AI, cyber risk and security, third-party risks, and ESG. This momentum is expected to carry forward into 2025 as regulations continue to evolve in critical areas such as Trusted AI and Systems, Cybersecurity and Information Protection, Financial and Operational Resilience, Financial Crime, Markets and Competition, and Risk Governance and Controls. Alongside new regulations like Digital Operational Resilience Act (DORA), NIS2, and the EU AI Act, organizations must also prepare for emerging regulations such as the Cyber Incident Reporting for Critical Infrastructure Act (CIRCIA), various US state data privacy laws, the EU Cyber Solidarity Act, the updated EU Product Liability Directive, the Corporate Sustainability Reporting Directive (CSRD), and the EU Deforestation Regulation.

Given the ever-increasing regulatory requirements, compliance teams inevitably fall behind. They spend most of their time tracking relevant regulations, understanding their impact on organizational processes, functions, risks, policies, and controls, implementing the required changes, and so on. Technology can make a huge difference in how these various compliance management tasks are performed.

Automated compliance is the future! Today, there are tools that leverage AI to scan the regulatory horizon for identifying relevant regulations and regulatory updates, quickly show the impacted processes, functions, risks, policies, and controls using a centralized platform, run autonomous control tests to ensure adherence to relevant regulations, generate reports that demonstrate compliance posture, and more. The technology-driven, automated approach can streamline compliance management activities and help strengthen compliance resilience.

Check out our eBook: Compliance Excellence: Top Strategies To Navigate The Regulatory Landscape

With its ability to provide actionable insights, save time and costs, and create bandwidth for risk, compliance, audit, security, and sustainability teams, AI is already being regarded as a game-changer for GRC. While AI will not completely replace the need for human involvement, it can eliminate the possibility of human error, thereby improving the accuracy of GRC processes and decision-making and ensuring there are no blind spots.

At the same time, it is essential to ensure responsible AI innovation. As organizations explore more use cases and integrate AI capabilities into their processes, they also have the duty to follow the highest standards to ensure its ethical and responsible use and implement measures to identify, manage, and manage AI risks. Think GRC for AI, if you will.

Regulators and standard-setting bodies have already taken steps toward this goal. The landmark EU AI Act will regulate AI in the EU by 2026. However, its reach will extend beyond the EU and affect more than just tech companies. In the US, the White House Office of Science and Technology Policy has formulated the Blueprint for an AI Bill of Rights. Other countries like the UK, Singapore, Australia, and India have also issued their own guidelines or principles around responsible AI.

To ensure responsible AI adoption, organizations should establish clear governance frameworks, conduct comprehensive risk assessments, promote transparency, monitor AI systems continuously, appoint accountable leadership, form cross-functional ethics committees, and educate employees on AI risks and compliance. These measures help align AI initiatives with ethical standards, legal requirements, and industry best practices.

AI-focused innovation has been central to MetricStream’s product and platform releases over the years. Our AI capabilities span diverse GRC use cases – from issue identification and classification, action plan recommendations, and scanning of SOC2 and SOC3 reports submitted to organizations by third parties, to , AiSPIRE, an AI-based knowledge-centric tool that provides intelligent insights to improve an organization’s control environment.

Read our latest eBook on the topic: AI: The Next Frontier in GRC

In 2024, cyber and operational resilience emerged as critical focal points for regulators and organizations, driven by an increasingly severe risk landscape. Disruptions caused by extreme climate events, geopolitical tensions, and IT outages underscored the urgency of building resilience to ensure quick recovery. Key regulations like the EU’s DORA for cyber resilience and the UK’s operational resilience policies from the Bank of England (BoE), Financial Conduct Authority (FCA), and Prudential Regulation Authority (PRA), highlight this growing emphasis. In the US, the Federal Reserve Board (FRB), Office of the Comptroller of the Currency (OCC), and Federal Deposit Insurance Corporation (FDIC) released a joint paper on operational resilience, while the Securities and Exchange Commission (SEC) mandated increased transparency around cybersecurity incidents. Globally, similar frameworks, such as Singapore’s guidelines, Hong Kong’s policy manual, and Canada’s Guideline E-21, reflect a universal recognition of the need for resilience in the face of operational and cyber threats.

Building robust resilience requires a well-structured operational risk management (ORM) program, as noted by the Basel Committee on Banking Supervision, which links operational resilience to effective ORM. Organizations must align their operational risk appetites and impact tolerances with resilience strategies, utilizing scenario planning, simulations, and proactive incident response testing. At the same time, cyber resilience will remain a top priority due to rising cyber threats and regulations like the EU’s Cyber Resilience Act (CRA). By fostering a culture of cybersecurity awareness and maintaining continuous risk monitoring, organizations can better protect their operations, minimize disruptions, and preserve stakeholder trust.

Explore more in the article: Operational Resilience: The Outcome of an Effective ORM Program

I’d like to close with two of my mother’s favorite quotes: “The perfect is the enemy of the good” and “A stitch in time saves nine.”

The first one she said so often I thought it was hers, but it’s a quote from 18th-century French philosopher and writer Voltaire. I use it all the time – don’t wait for perfection to start, and don’t let lack of perfection slow you down. The time to start improving your GRC journey is now.

The second quote also speaks to starting now and getting ahead: be proactive, not reactive. And I think it really was hers. Thanks, Mom!

Need help on your GRC Journey? Request a personalized demo today.

And… Happy New Year!

Artificial Intelligence (AI) technologies are rapidly transforming the landscape for risk and compliance professionals worldwide. According to a recent survey conducted by Moody’s, involving 550 global risk and compliance experts, 70% of respondents anticipate that AI will have a significant impact on the field within the next three years. Moreover, nearly 90% expressed a strong interest in integrating AI tools into risk and compliance solutions. Among the key applications, Generative AI (Gen AI) stands out as a transformative force in the field of Governance Risk and Compliance (GRC), particularly in policy and document management, offering the potential to streamline processes and enhance efficiency.

Policy creation in GRC is crucial for ensuring compliance with regulatory requirements and mitigating risks. It establishes a structured framework for governance, aligning organizational processes with industry standards while fostering accountability and transparency. Clear policies define roles, responsibilities, and acceptable practices, helping organizations address vulnerabilities and safeguard against legal, financial, and reputational risks. Additionally, well-crafted policies enhance audit readiness, support continuous improvement, and strengthen overall organizational resilience. AI can further enhance the role of policy management across the organization.

By infusing AI in policy management such as content drafting, grammar optimization, smart policy searches and predictive text suggestions, Gen AI streamlines these tasks by analyzing regulations, generating standardized templates, harmonizing stakeholder inputs, ensuring precise language, and tailoring policies to industry and regional needs. It also assists with cross-referencing existing policies, tracking changes, and enhancing audit readiness, saving time while boosting accuracy and scalability in policy creation. Let’s delve into how Gen AI is shaping the future of Policy and Document Management.

The initial stages of document creation often pose the biggest challenges. Starting from scratch requires significant time, effort, and expertise. Gen AI’s “Help me write” feature is designed to overcome this hurdle by assisting users in generating content quickly and efficiently.

Here’s how it works:

When multiple users contribute to a policy, generative AI can automatically summarize the content, ensuring clarity and coherence. It identifies key points, eliminates redundancies, and highlights critical changes, creating a concise overview of the policy. This helps streamline collaboration, improve version control, and provide a unified understanding of the policy's current state for all stakeholders.

Generative AI is revolutionizing policy and document management by making it more efficient, accurate, and adaptable. From simplifying the drafting process to ensuring compliance with evolving regulations, these tools are invaluable for organizations aiming to maintain high standards and productivity. By leveraging AI-driven solutions, companies can not only enhance the quality of their documentation but also foster a culture of innovation and agility. As this technology evolves, its potential to transform workflows and empower users will continue to grow, making it an indispensable part of modern document management strategies

MetricStream offers a robust policy and document management solution that integrates cutting-edge AI capabilities to enhance efficiency, compliance, and collaboration for effective policy management. Transform your approach to policy and document management with:

Request a demo now and find out how MetricStream’s Policy and Document Management solution, can transform your approach to GRC, ensuring resilience and agility in today’s complex regulatory landscape.

In July this year, the Microsoft-CrowdStrike IT outage brought the world to a standstill. Flights were grounded, banks were knocked offline, stock markets were disrupted, and healthcare systems were paralyzed for several hours – all because of a faulty software update.

This wasn’t the first time an operational failure caused such widespread disruption.

In 2018, an IT outage at British Bank, TSB, left nearly two million customers locked out of their accounts. A year earlier, the NotPetya cyberattack devastated the systems of some of the world’s biggest corporations, while WannaCry ransomware cost the UK’s National Health Service (NHS) a whopping £92 million after 19,000 appointments were canceled.

Then, of course, came the pandemic which upended life as we knew it. Organizations were forced to suddenly adapt to remote work, scale up digital services in days, and navigate supply chain disruptions – all while facing an unprecedented threat to human health.

Thankfully, the worst of the pandemic is behind us. But it won’t be the last major crisis we face. Risks are growing in volume, velocity, and interconnectedness. Simultaneously, cyber threats and vulnerabilities across legacy systems, new technologies, and third parties are constantly evolving.

So, when another disruption does occur – because it will – what can organizations do to withstand, adapt to, and recover from it faster?

Operational resilience isn’t a new concept – it’s been on the regulatory radar for years. In 2018, the Bank of England, UK’s Prudential Regulation Authority, and Financial Conduct Authority published a joint discussion paper on how to improve the operational resilience of firms and financial market infrastructures.

That was followed in 2021 by the Basel Committee on Banking Supervision’s (BCBS’s) ‘Principles for Operational Resilience’. The Principles assert that while it may not be possible to avoid certain operational risks like a pandemic, it’s certainly possible to improve one’s resilience to such events.

Resilience is about building the capacity to anticipate, respond to, and bounce back from a disruption with minimum damage. It doesn’t just involve backing up data, or establishing emergency protocols – it also focuses on preventing and detecting potential issues before they escalate.

Resilient organizations are better-prepared for eventualities in both the short and long term. They have robust business continuity, incident management, and recovery plans in place. More importantly, they’re proactive about assessing, monitoring, and mitigating operational risks – thereby, lowering the likelihood of a disruption even occurring.

With operational resilience becoming increasingly critical to the health of organizations and industries at large, a host of new regulations around the subject have emerged:

While each of these regulations has its own set of requirements, the one aspect many of them share is a focus on operational risk management (ORM) as a key driver of operational resilience.

At the 2019 Annual Operational Risk Europe Conference in London, the then Director of the Supervisory Risk Specialists, Nick Strange, said, “…operational resilience is the outcome we are seeking, and to do that we must manage operational risk effectively.”

BCBS echoed this sentiment in their Principles saying, “Operational resilience is an outcome that benefits from the effective management of operational risk.”

If that’s the case, how can organizations manage operational risks better?

MetricStream Operational Risk Management provides a comprehensive set of capabilities to identify, assess, mitigate, monitor, and report operational risks. Packed with powerful risk quantification tools and analytics, our ORM software delivers a single, real-time view of risks and controls to help you make risk-informed decisions. With MetricStream, you can establish a strong ORM framework, manage RCSAs with ease, and stay ahead of potential losses with predictive risk indicators.

Our MetricStream Operational Resilience Management software provides a single view of risk insights across operational risk, business continuity, third-party, and cybersecurity risk areas. With automated workflows and real-time reporting capabilities, the operational resilience software embeds risk management into business continuity and crisis recovery processes. So, you can efficiently anticipate, tolerate, and bounce back faster from an adverse event.

Ready to find out more? Request a personalized demo now.

At the recently held GRC Summit 2024 in Baltimore, David Story, Vice President Health, Safety, & Environment, dnata, provided the audience with a detailed overview of their GRC journey experience with MetricStream.

Dubai National Air Travel Agency (or dnata) was established in 1959 through a government decree. It set up its first international business in 1993. Gradually, over the years, it has seen significant growth across all its business units.

Here are the excerpts from David’s session on “dnata’s Integrated GRC Transformation”.

David: Our foremost priority is safety and security. Through a series of SMART objectives, we're building a best-in-class, health, safety, and environmental system, or HSE ecosystem, as we call it. Over the next few years, up to 2027 and beyond, through our medium-term plan, we are striving for a best-in-class or world-class status, and central to delivering on that goal is the effective use of our GRC platform.

Within dnata, MetricStream is the product that we use, and we have done a number of modifications and upgrades through MetricStream over the years. We refer to it within the company as “dnatahub”, which is everything we do from a GRC perspective.

So, in terms of why GRC is so important to us -- central to that is our safety management system, or SMS. SMS is essentially the bedrock of everything that we do across four key pillars -- safety policy, risk management, assurance, and promotion. To be able to deliver on the requirements of our SMS, our dnatahub platform is absolutely central to achieving those goals.

David: So, how has the dnatahub platform evolved over the last few years?

We're now into the 9th year of our partnership with MetricStream, beginning back in 2015 along with our “Global One Safety” initiative. The first pillar in that strategy was rolling out Incident Management, which allowed us to have one platform for reporting safety occurrences across local businesses.

In 2018, there was global expansion – we introduced new applications within dnata in addition to incident management and reporting.

In 2020, we started moving into the continuous monitoring phase, which saw the likes of our Documentation Management System (DMS). We also introduced surveys and inspection through the auditors. We would go out there and report safety hazards and threats to our organization. This was across all three of our operational divisions.

The beauty of DMS is that it can be accessed by any of our team in the world who got access to Office 365 accounts. Examples of a DMS document could be a global safety alert, a new manual, a guideline document, or a new operational standard. All of those are published through DMS and are automatically and electronically tested within the system as well. So, for auditing purposes, it's very, very efficient.

We also launched Observation Management as well. And, through Issue and Action Management we can assign tasks and actions to our businesses around the world.

We're now moving into Phase IV, as we call it, looking at how we scale up as we continue to build our business. We are currently two weeks away from the launch of the Euphrates upgrade as well.

We've built a very strong partnership with MetricStream, and we've now established a very strong governance model as well in terms of performance monitoring.

David: What's been key to success is keeping things simple. One of the worst things you can do in my role as a safety professional is over-complicate how you manage safety within your business.

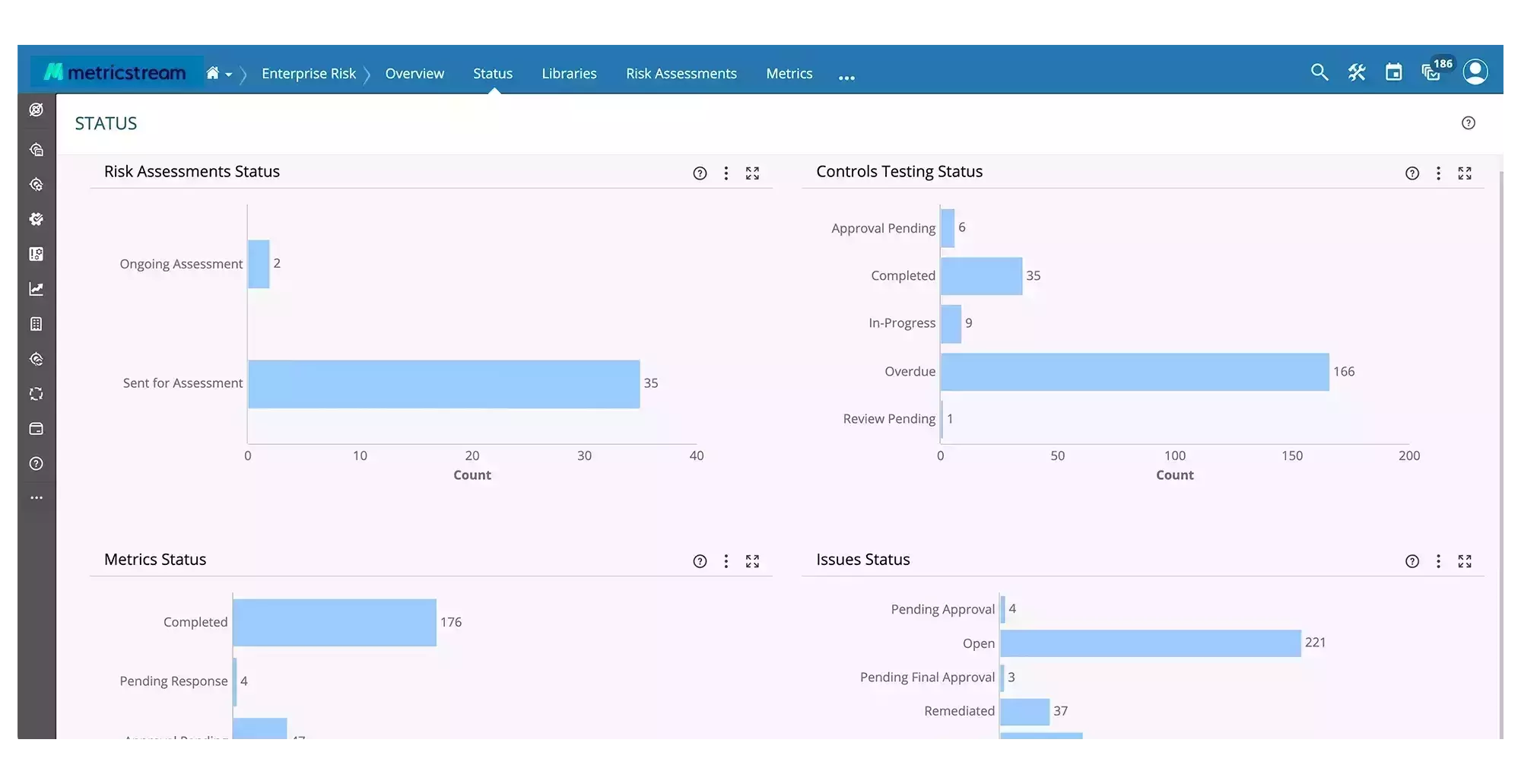

In terms of just some numbers, we have got:

What gives me great confidence is 400,000+ observations. We actively encourage -- from our leadership level all the way down to the front line -- to report any unsafe behaviors and actions within our business. What we've seen over the last 2-3 years is a considerable increase in the number of safety reports within the business. So that leads to a much more positive and safety-aware culture.

Over the next few years, we've got some really interesting challenges coming our way. You would have seen the announcement about the new airport project in Dubai. The target is 2033 for the opening of the new terminal with a capacity of 250 million passengers a year. We already have that airport as we have for the last 10 years, and this will be a significant upgrade to be the world's largest international gateway.

We have two to three new businesses that are going to be coming online towards the end of this year, including a particularly large business in Italy. And it's essential that we look at how we scale up to meet that demand, because we could have potentially 3,000 to 4,000 users within dnata by the end of this year.

Also Read:

In today’s global economy, where uncertainty is the only constant, savvy organisations treat risk as a strategic advantage. According to Aon’s 2025 Global Risk Management Survey, geopolitical volatility, cyber risk, and regulatory change have climbed into the top global risk rankings for the first time, underscoring the need for stronger ERM practices.

That’s where ERM tools come in - and why platforms like MetricStream matter. These tools provide organizations with the infrastructure to collect, analyze, and monitor risk data across the entire enterprise. By translating scattered risk signals into clear dashboards and actionable insights, they help leadership anticipate threats, prioritise mitigation, and steer strategy with confidence.

In 2026, as operational, cyber, and third-party exposures intensify, selecting the right ERM solution has become a critical priority for GRC leaders, CISOs, and risk professionals.

Use of modern ERM tools transforms risk management from a reactive chore into a proactive capability - centralising visibility over compliance, operational, strategic, and third-party risks so teams can act before issues escalate.

An ERM tool is software that centralises the identification, assessment, monitoring, and reporting of risks across an organisation. It collects risk data from business units, links exposures to strategy and controls, and presents actionable insights so leaders can prioritise and coordinate risk responses.

Here are some well-known vendors that are recognized as leaders in the ERM landscape.

MetricStream has carved its place as an indispensable ERM tool for businesses aiming to bolster their enterprise risk management capabilities. This ERM software is crafted with an eye for integrating various aspects of risk management under a single umbrella, making it a holistic platform for businesses aiming to stay ahead of uncertainties.

This tool is best suited for organizations seeking to streamline risk processes, gain real-time insights into their risk landscape, and drive informed decision-making to optimize business performance and resilience in dynamic environments.

Key Features:

MetricStream's accolades, such as being named a Leader in The Forrester Wave™: Governance, Risk, and Compliance Platforms, Q4 2023, highlight its effectiveness and reliability. Recognition from leading research and advisory firms attests to the platform's robust capabilities in IT/Cyber Risk Management, GRC Vision, and more

To read more, download your complimentary copy of The Forrester Wave™: Governance, Risk, and Compliance Platforms, Q4 2023.

Customer feedback — why users trust MetricStream

Diligent offers a compelling narrative for ERM, emphasizing the importance of aligning leadership with the full spectrum of risks that impact an organization.

This strategic alignment is pivotal in transforming risk into actionable insights, enabling data-driven decision-making at every turn.

Diligent's approach revolves around cultivating a much more comprehensive understanding of risks across all levels of the organization, fostering a proactive risk management culture.

Key Features:

Pricing will be available on request to the vendors.

ServiceNow is a robust platform that simplifies complex risk assessments and enhances decision-making capabilities across organizations.

It facilitates enhanced data communication using chat functionalities, web portals, and mobile applications, ensuring seamless sharing and dissemination of critical risk and compliance information across the organization.

This platform is ideal for organizations looking to centralize and optimize their risk management processes while enhancing overall operational resilience.

Key Features:

Custom pricing will be available on request.

OneTrust is a comprehensive tool that specializes in compliance and vendor risk management, addressing critical niches within the risk management ecosystem. This tool is particularly valuable today, where data privacy regulations and third-party relationships are under increased scrutiny.

It has made its mark as a versatile cloud-based GRC platform, renowned for its customizable functionalities that cater to a wide range of risk management needs.

Key Features:

Pricing will be available on request.

LogicGate presents itself as a highly adaptive and modern ERM solution designed to meet the dynamic needs of contemporary businesses.

Known for its flexibility and the ease with which it can be customized, LogicGate stands as a powerful tool in any risk manager's arsenal, particularly for those looking to streamline their ERM processes without being bogged down by complex technical requirements.

With LogicGate, businesses can forge ahead confidently, equipped with a versatile platform that aligns seamlessly with their risk management goals and operational strategies.

Key Features:

Pricing will be available on request to the vendors.

1. Consolidate risk information across the enterprise

An ERM tool pulls risk data from different teams into one place. Instead of juggling spreadsheets or chasing updates, you get a clear picture of what the organisation is facing and where the pressure points are.

2. Quantify risk impact and likelihood

Good tools help translate concerns into measurable terms. You can see how big a risk truly is, what it might cost, and how likely it is to materialise—making comparisons and decisions far more grounded.

3. Predict emerging risks through analytics

Modern ERM platforms spot patterns that teams may miss. Early signals, trends, and shifting conditions become easier to detect, giving leaders more time to respond.

4. Support informed, data-led decisions

By connecting risks to business goals and controlling performance, ERM tools help leaders decide where to act and where to invest. Choices become clearer, faster, and easier to justify.

5. Strengthen organisational resilience

With better visibility and more timely insights, organisations can respond to shocks with less disruption. ERM tools help teams prepare, adapt, and stay steady even when conditions change suddenly.

Here are the key features that CROs and risk managers should keep in mind while selecting an ERM tool:

Here are some ways in which efficient ERM tools help support regulatory compliance:

When evaluating ERM tools, prioritize ease of use with intuitive interfaces that encourage user adoption. Consider the ROI beyond upfront costs, aiming for reduced risk event losses and improved efficiency. Assess functionality for alignment with specific needs, such as configurable risk assessments and reporting. Lastly, prioritize integration capabilities for smooth connectivity with existing platforms.

Gauging the success of your ERM implementation involves reviewing a range of criteria that validate its benefits. with some of them being:

Implementing an ERM tool brings a host of advantages to organizations seeking to enhance their risk management practices. Here are the top four benefits of using an ERM tool:

Implementing ERM tools enables organizations to peel back the layers of potential risks, revealing unseen threats and opportunities alike. This clarity enables businesses to anticipate challenges and navigate them with greater assurance.

With the insights garnered from these tools, organizations can make better-informed decisions that align closely with their goals. ERM tool offers the unique advantage of data-driven guidance, helping firms to allocate their resources more effectively, and ensuring that efforts are directed toward areas of highest impact.

ERM tools empower organizations with a proactive defense mechanism against potential disruptions. This robust preparedness doesn’t just mitigate risks, it also fosters an agile environment that can adapt and thrive in the face of uncertainties.

ERM tools serve as an invaluable ally, ensuring that compliance is maintained, and governance standards are met. This compliance is a strategic move that enhances credibility and stakeholder trust, paving the way for smoother operations and market growth.

Below is a concise, accurate comparison of five leading platforms across a few practical dimensions:

| Platform | Risk Analytics | Automation | Dashboard | Integration | Best For |

| MetricStream | Enterprise-grade analytics with built-in risk scoring, scenario and trend analysis. | Mature workflow automation for assessments, issues, and remediation at scale. | Executive and operational dashboards with deep drill-down for regulators and C-suite. | Prebuilt connectors to finance, IT, security, and ERP stacks; strong API support. | Large regulated organisations (banking, healthcare, energy) needing end-to-end GRC. |

| Diligent | Board and enterprise risk insights with benchmarking and analytics focused on governance metrics. | Workflow automation for policy, meeting packs, and compliance tasks. | Board-grade dashboards and risk reporting designed for directors and executives. | Integrates with BI, document management, and common enterprise systems. | Organisations that prioritise board reporting, governance, and executive oversight. |

| ServiceNow | Operational risk analytics via Performance Analytics and integrated risk workbench. | Best-in-class automation and orchestration for risk workflows and IT-driven processes. | Real-time operational dashboards built into the Now platform. | Extensive ecosystem: ITSM, CMDB, SIEM, ERP, HR systems and broad enterprise connectors. | Enterprises that need deep workflow automation and strong IT risk linkage. |

| OneTrust | Analytics designed for privacy, third-party and IT risk with regulatory mapping. | Automated assessments, questionnaires, consent and vendor lifecycle workflows. | Customisable compliance and privacy dashboards with risk heatmaps. | Large integration catalog for HR, cloud apps, security feeds, and vendor APIs. | Organisations focused on privacy, third-party risk, and regulatory compliance. |

| LogicGate (Risk Cloud) | Flexible, real-time risk insights with configurable scoring and report builders. | No-code automation and workflow builder for rapid process automation. | Configurable operational dashboards that non-technical teams can adapt. | Ready integrations for Jira, Snowflake, Workday, SIEMs and common data stores. | Mid-to-large organisations seeking fast configuration and strong automation. |

Implementing ERM tools presents unique challenges that organizations must strategically address to ensure successful adoption and integration. From overcoming resistance to change and data quality issues to promoting cross-functional collaboration and enhancing risk assessment processes, navigating these challenges is essential for maximizing the effectiveness of ERM tools within companies.

Implementing ERM tools often requires changes in workflows and processes, which can be met with resistance from employees accustomed to traditional methods. Overcoming resistance to change involves effective change management strategies, such as stakeholder engagement, training programs, and transparent communication about its benefits.

ERM tools rely heavily on accurate and reliable data to perform effective risk assessments and analyses. However, organizations may often struggle with data quality issues, including incomplete or outdated information, inconsistent data formats, and data silos.

Different departments often have narrow views of risk that don't account for how their risks might impact the rest of the organization. Organizations need to promote a culture of collaboration and an understanding of the interconnectedness of risks by establishing cross-functional risk committees and information-sharing protocols.

Organizations need to assess risks timely, systematically, and objectively to strengthen risk preparedness and to be ready for the unexpected curveballs waiting to surface at the most inconvenient times. This requires developing comprehensive methodologies that consider risk likelihood, impact, velocity, and interconnectivity. Furthermore, organizations should update their risk profile regularly as conditions change.

Stakeholders can't make good risk-based decisions without timely and relevant information. It is imperative to establish risk reporting procedures to keep executives and risk owners in the loop. A risk dashboard or scorecard is a useful way to provide at-a-glance overviews and details on key risks.

Determining the success of your ERM implementation entails examining critical factors that showcase its achievements and improvements, such as:

Here are some of the latest trends that companies can look forward to, when it comes to boosting the effectiveness of ERM tools.

As we look forward to the trends of 2025, it’s clear that the future of ERM is not just about navigating uncertainties but about thriving in them. And when it comes to turning risks into rewards, MetricStream is a trusted partner, equipped to tackle the future of risk-management head-on.

To learn how MetricStream Enterprise Risk Management can help, request a personalized demo today.

An ERM tool is software that helps organizations identify, assess, manage, and monitor risks across the enterprise. It centralizes risk data, streamlines workflows, and provides real-time visibility into the organization’s overall risk posture.

Organizations use ERM tools to break down silos, improve risk transparency, automate assessments, and make risk management more consistent and data-driven. These tools also help strengthen compliance, reduce operational surprises, and support strategic planning.

The most important features include risk scoring and analytics, dashboards and reporting, control monitoring, issue and incident tracking, integrations, workflow automation, and the ability to map risks to controls, assets, and regulations.

ERM tools turn scattered risk data into clear insights, helping leaders understand which risks matter most and why. They support better prioritization, align risks with business impact, and provide evidence-based guidance for allocating resources.

Top ERM tools include MetricStream, LogicGate, Resolver, AuditBoard, and Archer. These platforms stand out for strong analytics, flexible workflows, and support for integrated risk management programs.

Start by defining your risk goals, maturity level, and workflows. Then compare tools based on usability, configurability, reporting, integrations, customer support, and scalability. Pilots, demos, and customer reviews also help clarify the best fit.

Industries with complex, fast-changing risk environments benefit the most—such as financial services, manufacturing, healthcare, energy, technology, government, and retail. These sectors rely on ERM tools to manage regulatory demands, cybersecurity threats, operational risks, and third-party exposure.

ERM tools focus primarily on identifying, assessing, and monitoring enterprise-wide risks. GRC suites are broader and include governance management, compliance tracking, audit workflows, and policy management. ERM is often a core module within a larger GRC platform.

They connect risk exposure to business objectives and financial impact. Scenario analysis and aggregated dashboards help leadership evaluate trade-offs. This enables informed choices about growth, investment, and resilience.

Scalability depends on architecture rather than brand alone. Enterprise-grade platforms with modular design, multi-language support, and regional regulatory mapping tend to scale best. Cloud-native systems often provide greater flexibility for global operations.

Integration allows risk data to flow from security tools, finance systems, and operational platforms into a single view. Without integration, risk insights remain fragmented. Strong APIs reduce manual work and improve real-time visibility.

Some platforms provide industry templates, regulatory libraries, and preconfigured risk taxonomies. Financial services, healthcare, and energy sectors often require specialized reporting and compliance features. However, many enterprise tools can be configured to meet sector-specific needs.

Poor data quality and unclear ownership can weaken adoption. Over-customization may increase complexity and cost. Lack of executive sponsorship often limits long-term impact.

They centralize control documentation, testing results, and remediation tracking. Automated reporting and evidence collection simplify audit preparation. Clear audit trails strengthen defensibility during regulatory reviews.